A deed in lieu of foreclosure is when you give your home’s deed to your lender to avoid foreclosure. It can help you move on faster. However, it impacts your credit score. This guide explains how it works, its pros and cons, and other options.

Key Takeaways

- A "deed in lieu of foreclosure" lets you give your home to your lender. This avoids a full foreclosure fight.

- It protects your privacy and is less stressful than foreclosure. It also costs less and is faster.

- The process involves contacting your lender, applying, and transferring the deed.

- A deed in lieu harms your credit score. However, it is usually less damaging than a full foreclosure.

- You may still owe money (a "deficiency") after a deed in lieu. Try to get your lender to forgive this debt.

- Other options include short sales, loan changes, and repayment plans.

What Is a Deed in Lieu of Foreclosure?

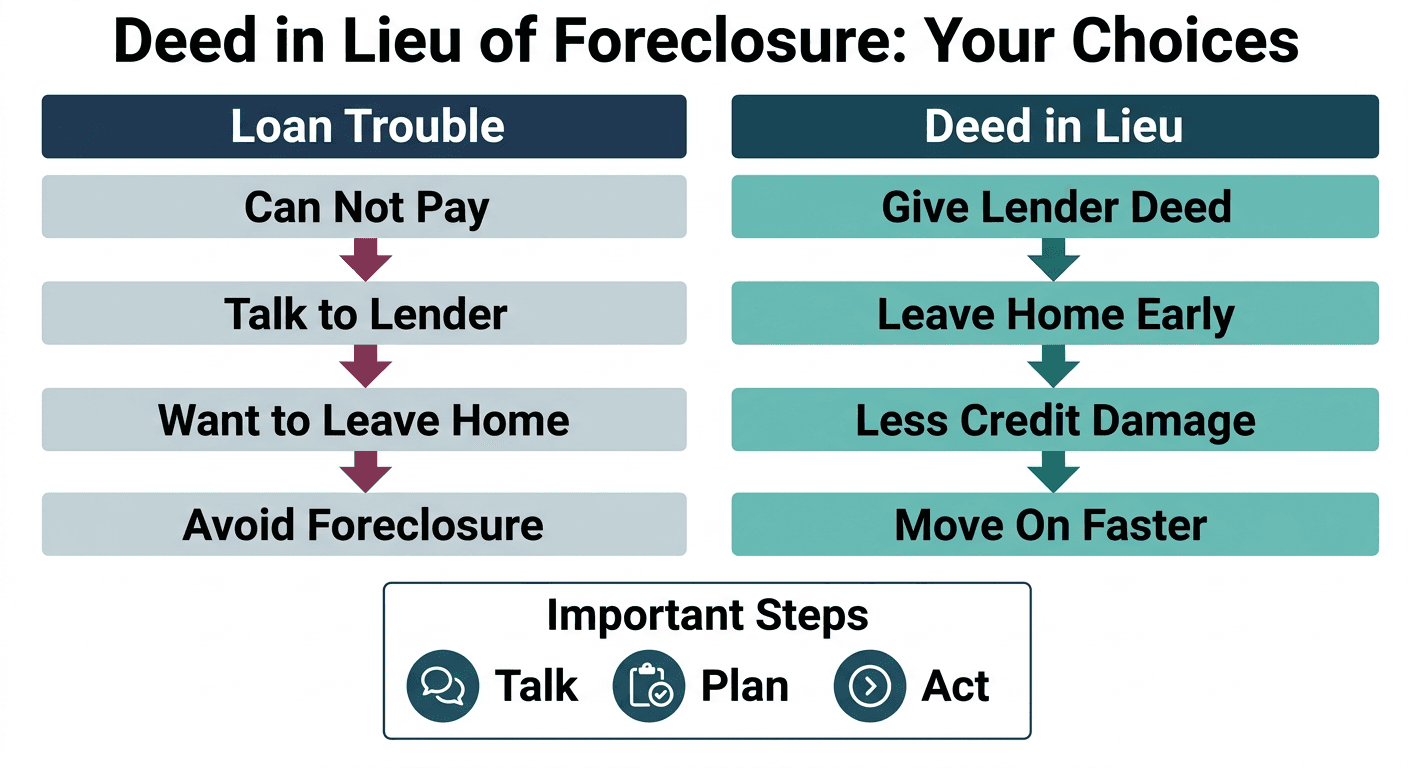

A deed in lieu of foreclosure lets you give your home back to the bank to avoid a long and public foreclosure. A "deed in lieu of foreclosure" is a special deal. You willingly give your home's ownership (the deed) to your mortgage lender. This happens when you cannot make your payments anymore. This option helps you avoid a full foreclosure. Foreclosure is when the bank takes your home through court. Giving the deed in lieu helps everyone skip that long, costly legal fight. It is your choice, not something the bank forces on you. You might choose this if you face money problems. Examples include losing your job or having big medical bills. It can help you move on from a home you cannot afford. Our blog has more information on selling a house fast for cash. Here’s what it means in simple terms:- Deed: This is the legal paper proving you own your home.

- In Lieu Of: This means "instead of."

- Foreclosure: This is when the bank takes your home because you failed to pay.

Why Consider a Deed in Lieu?

A deed in lieu can help you avoid the public and costly process of foreclosure. A deed in lieu of foreclosure offers several benefits. It can help you move on without a long, public foreclosure. This option saves you from legal fees and stress. Plus, it usually closes faster than a full foreclosure. Here are some key benefits:- Privacy: Foreclosures become public records. A deed in lieu keeps your hardship more private. This means fewer public notices about your money troubles.

- Less Stress: The foreclosure process is often long and stressful. A deed in lieu can offer a quicker, simpler fix. This reduces worry and uncertainty.

- Lower Costs: Foreclosures involve many legal and admin fees. With a deed in lieu, you generally avoid these extra costs. This saves you money in a tough time.

- Faster Process: A regular foreclosure can take months. In some states, it can take over a year. A deed in lieu can often be done much faster. This lets you fix the issue and move forward. For example, a foreclosure may take 12 to 18 months, but a deed in lieu often wraps up in 3 to 6 months.

How Does a Deed in Lieu Work?

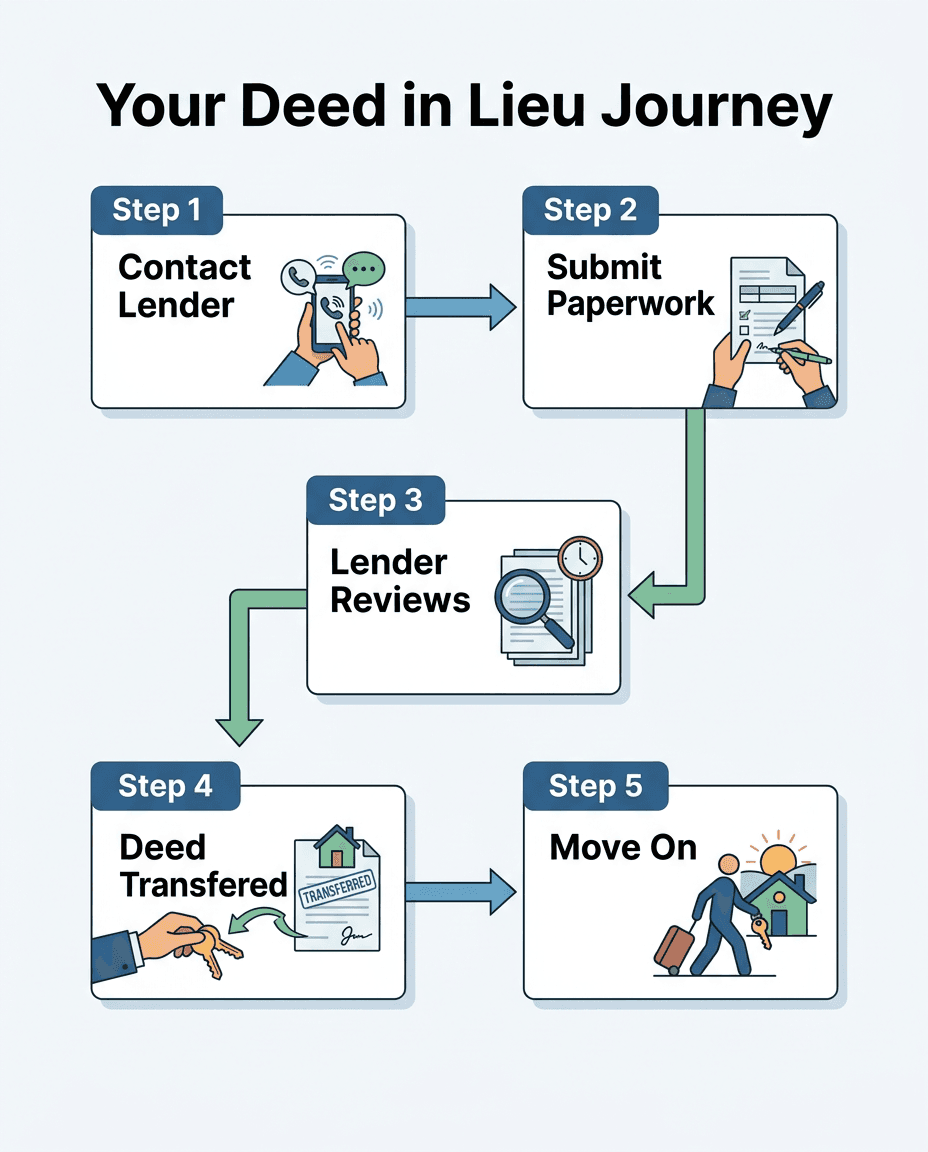

A deed in lieu lets you give your home back to the lender to avoid foreclosure. You might consider a deed in lieu if paying your mortgage is hard. This process involves talking with your lender. You show them you want to give up the home. Then, you transfer its ownership to them. Here is how a deed in lieu process often works:- Step 1: Contact Your Lender. This is the first and most important step. Tell your lender you cannot make your payments. Ask about options to avoid foreclosure, like a deed in lieu. Being open and honest is important for homeowners.

- Step 2: Submit an Application. Your lender will likely ask you to fill out forms. These forms show your money troubles. You will need papers like pay stubs, bank statements, and tax returns. This helps the lender see your full picture.

- Step 3: Lender Review. The lender checks your application. They look at your home's value. They also check if other debts are tied to it. They decide if accepting the deed in lieu is better for them than a full foreclosure.

- Step 4: Agree to Terms. If approved, you and the lender make a deal. This is a formal contract. It explains what happens next.

- Step 5: Transfer the Deed. You sign papers that move your home's ownership to the lender. This deed transfer usually happens at a title company.

What is the Difference Between a Deed in Lieu and Foreclosure?

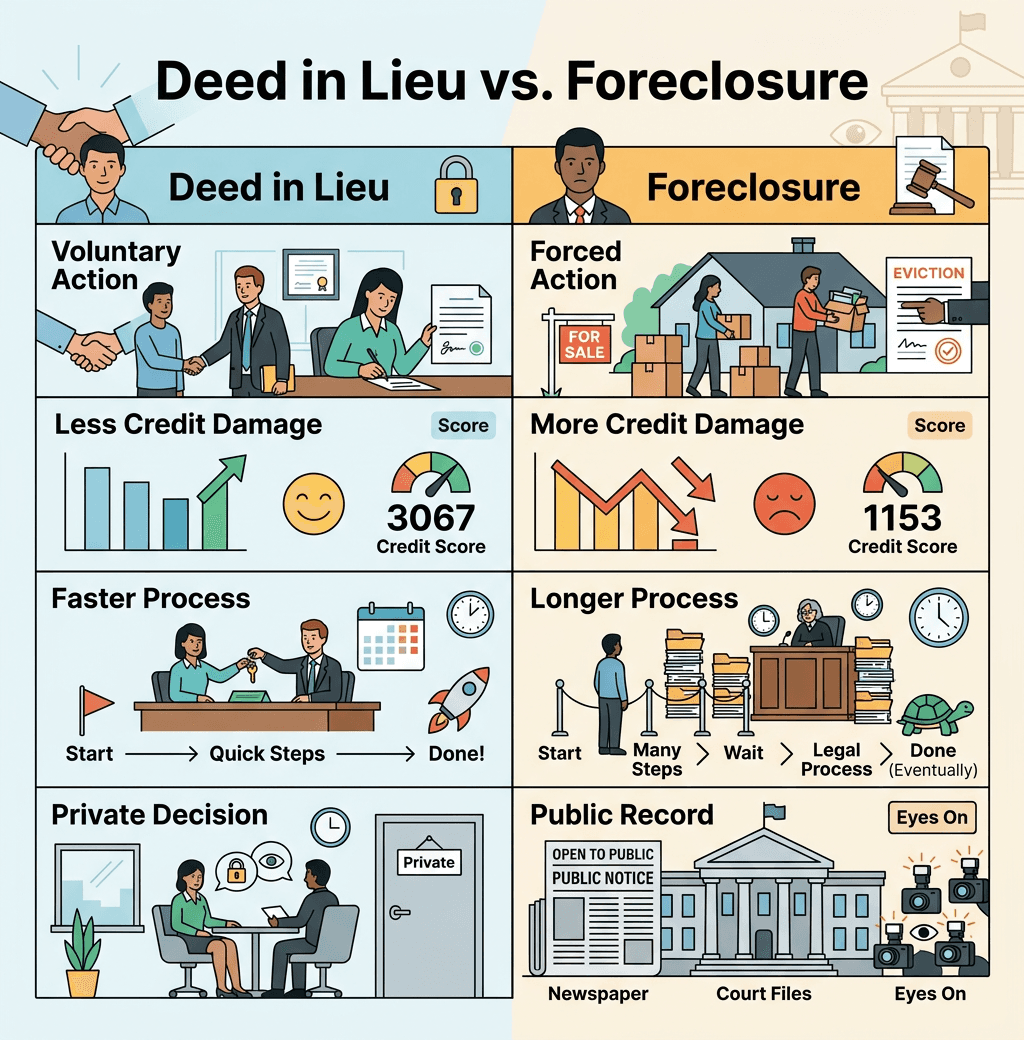

A deed in lieu differs from foreclosure mainly in how voluntary and public the process is, and how it impacts your credit.

Comparison table showing differences between a deed in lieu of foreclosure and traditional foreclosure.

A deed in lieu happens when you and your lender agree that you will give them your home. This is a voluntary choice. You sign over the property deed to your lender. This avoids a long, costly legal fight.

Foreclosure is when your lender takes your home through a legal process. This happens if you stop making mortgage payments. It is not voluntary. Your lender must follow strict rules in court.

Here are the main differences:

- Choice:

- Deed in Lieu: You choose to give up your home to the lender.

- Foreclosure: The lender forces you to give up your home.

- Legal Process:

- Deed in Lieu: It is a faster process. You avoid court costs.

- Foreclosure: It is a long, public court process. This costs both you and the lender time and money.

- Public Record:

- Deed in Lieu: This is less public. It may not get as much attention.

- Foreclosure: This is a public record. It often stays on your credit report longer.

- Credit Impact:

- Deed in Lieu: Generally, this is less damaging to your credit score than a foreclosure. It shows you tried to work with your lender.

- Foreclosure: This is very bad for your credit score. It can stay on your report for seven years. Losing your home through foreclosure can drop your score by over 100 points.

How Bad Does a Deed in Lieu of Foreclosure Hurt Your Credit?

A deed in lieu hurts your credit, but often less than a full foreclosure. A deed in lieu will lower your credit score. Lenders report it to credit bureaus as "deed in lieu of foreclosure." This record shows you did not pay back your loan as agreed. Your credit score could drop by 50 to 150 points. The exact drop depends on your score before the deed in lieu. This is usually better than a full foreclosure. A foreclosure often causes a larger drop, sometimes 100 to 200 points. A deed in lieu shows you worked with your lender. This looks slightly better on your credit report. You may still face a waiting period for new mortgages. This can be two to four years, compared to seven years for foreclosure. You can rebuild your credit after a deed in lieu. Follow these steps:- Check your report. Get a free copy of your credit report each year. Make sure the record is correct.

- Pay bills on time. Always pay other debts, like credit cards, on their due dates. This shows you are a reliable borrower.

- Keep old accounts. Do not close old credit cards. A longer credit history helps your score.

- Use credit wisely. Keep your credit card balances low. Try to use less than 30% of your available credit. For example, if you have a card with a $1,000 limit, keep your balance under $300.

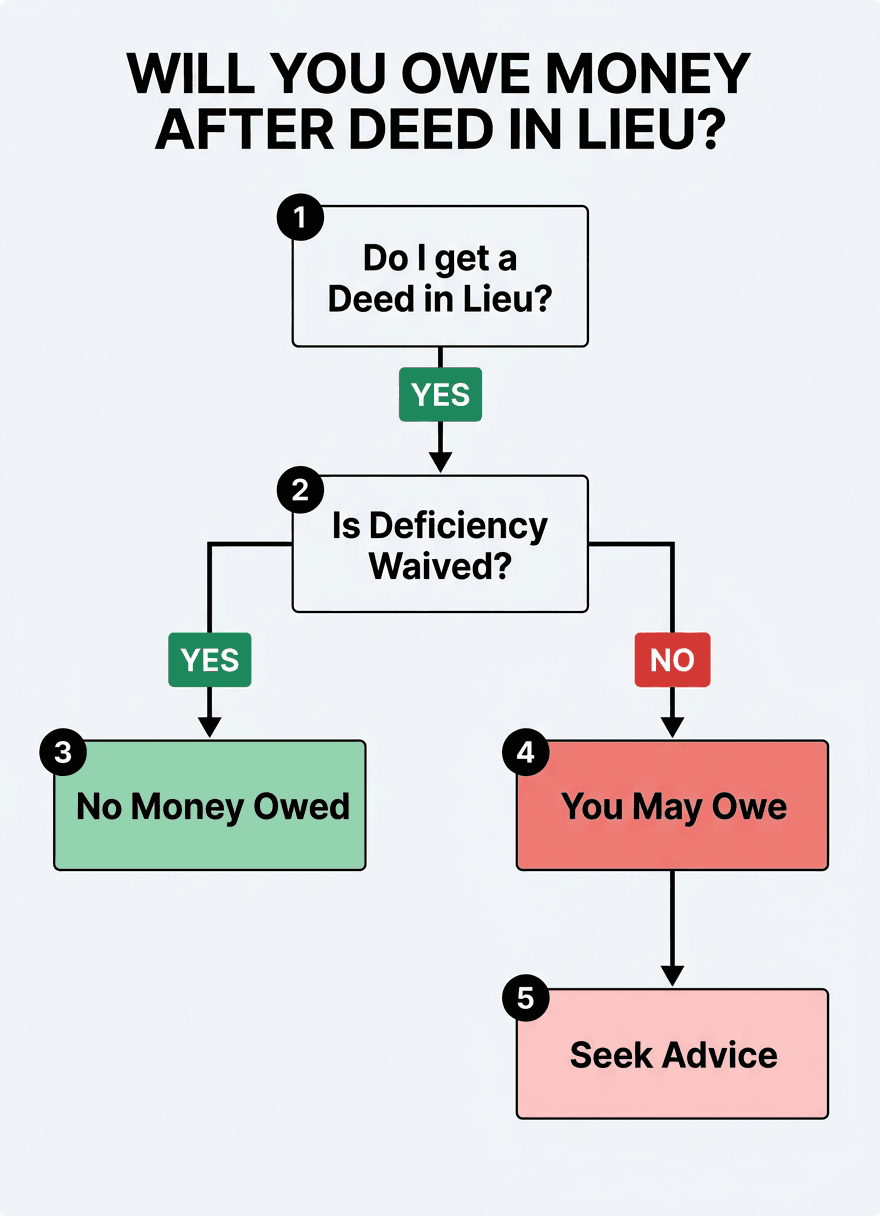

Will I Owe Money After a Deed in Lieu of Foreclosure?

You may still owe money after a deed in lieu of foreclosure, but you can often avoid it. Giving your deed to the bank can feel like the end. But sometimes, you might still owe money. This is called a "deficiency." It happens when your home sells for less than you owe on the mortgage. For example, if you owe $250,000 but the home is worth only $200,000, the $50,000 difference is the deficiency.

Flowchart explaining if a homeowner will owe money after a deed in lieu of foreclosure.

You can often avoid owing this money. Negotiate with your lender to waive (forgive) the deficiency. Get this agreement in writing before you sign anything. This protects you from future bills.

Be aware of tax rules. If your lender forgives a deficiency, the IRS might see this as income. This means you could owe taxes on that forgiven amount. For instance, if they forgive $50,000, that could be added to your taxable income.

Talk to a tax advisor or lawyer. They can help you understand your specific situation. They can explain any potential tax bills. They can also help you understand if you qualify for tax relief. Knowing these details helps you make the best choice.

Consider exploring different ways to sell your house fast if a deed in lieu or foreclosure is on your mind. Companies like HouseGoodbye.com can help you sell your Michigan home for cash. This often avoids the tough choices of foreclosure completely. Ask a tax professional about debt forgiveness rules if that applies to your situation.

Is a Deed in Lieu of Foreclosure Bad?

A deed in lieu can be a less damaging choice than a full foreclosure. Many people wonder if a deed in lieu of foreclosure is bad. It's true that giving up your home is never ideal. It affects your credit score. However, it is often less severe than a full foreclosure. For example, a deed in lieu might lower your score by 100-200 points. A foreclosure could drop it by 200-300 points or more. Think of it as choosing the "least bad" option when facing tough times. You avoid the stress of a long legal fight. You also prevent the public record of a foreclosure. This choice can help you move forward faster when you cannot make your mortgage payments. Sometimes, a deed in lieu is the best way to handle a difficult situation. It offers a cleaner break. This allows you to start rebuilding your financial standing sooner.Alternatives to Deed in Lieu of Foreclosure

If a deed in lieu isn't right for you, other ways exist to avoid foreclosure. You have choices if you cannot pay your mortgage. A deed in lieu of foreclosure is one option. But other paths can also help you avoid losing your home. Understanding these can help you decide the best step for your situation.Other Paths to Avoid Foreclosure

Many options can prevent foreclosure. The right choice depends on your financial state. It also depends on your lender's rules.- Short Sale: This means you sell your home for less than you owe on your mortgage. Your lender must agree to this sale. They accept the sale price as full payment.

- Benefit: You avoid foreclosure on your credit report.

- Drawback: It still harms your credit score. You also lose your home.

- Loan Modification: Your lender changes your mortgage terms. This could mean a lower interest rate. It might also mean longer payment times. This makes your monthly payments smaller.

- Benefit: You keep your home and make payments more easily.

- Drawback: It can take time to get approved.

- Repayment Plan: Your lender might let you pay back missed payments over time. You pay extra each month until you catch up.

- Benefit: You get to keep your home. You also catch up on payments.

- Drawback: Your monthly payment will be higher for a while.

- Forbearance: Your lender lets you stop making payments for a set time. This gives you time to improve your finances.

- Benefit: Gives you a break from payments when you need it.

- Drawback: You still owe the money. You will need to pay it back later.

What is the Best Option to Avoid Foreclosure?

The "best" option depends on your unique situation. If you want to keep your home, a loan modification or repayment plan is often better. If keeping the home is not possible, a short sale or deed in lieu may be better. Both let you avoid a public foreclosure record. Some homeowners choose to sell their house directly. Companies like HouseGoodbye.com buy houses quickly for cash. This can be a fast way to get out from under a mortgage. It also offers a fresh start. You won't have the worry of foreclosure. Learn more about selling your house fast for cash in specific areas, like selling your house fast in Ann Arbor, MI. The U.S. Department of Housing and Urban Development (HUD) offers counseling. They can help you understand your options better. You can find more information and resources on their official website about avoiding foreclosure. They can help you plan your next steps.Deed in Lieu vs. Short Sale: What's the Difference?

A deed in lieu and a short sale are both ways to avoid foreclosure, but they work in different ways. Let's look at what a short sale is first. In a short sale, you sell your house for less than you owe on the mortgage. Your lender must agree to this lower sale price. They then forgive the remaining loan amount. You still find a buyer, like with a normal sale. However, the bank approves the final deal. Here's how a deed in lieu differs from a short sale:- Property Transfer:

- Deed in Lieu: You give the house deed directly to your lender. You are no longer the owner.

- Short Sale: You sell your house to a new buyer. The sale itself pays off part of your loan.

- Approval Process:

- Deed in Lieu: The lender takes ownership. This avoids the long foreclosure process for them.

- Short Sale: The lender must approve the sale price. A buyer needs to be found. Often, a real estate agent helps. See how to sell a house without a Realtor.

- Credit Impact:

- Both options harm your credit score. A deed in lieu may be slightly less damaging than a foreclosure. A short sale might also look somewhat better than a full foreclosure on your credit report. Each lender reports these differently.

- Owed Money:

- With both options, the lender often agrees to forgive the debt difference. This means you won't owe money after the house is gone. Always get this agreement in writing.

Steps to Request a Deed in Lieu

Here's how to ask your lender for a deed in lieu of foreclosure.

Diagram showing the step-by-step process of requesting a deed in lieu of foreclosure.

If you face hardship and cannot pay your mortgage, reach out to your lender right away. Early action is key. Many lenders have special teams. They help homeowners avoid foreclosure.

Follow these steps to request a deed in lieu:

- Contact Your Lender: Call their customer service number. Clearly explain your money situation. Ask about their "loss mitigation" options. These are programs that help people keep homes or avoid foreclosure.

- Gather Documents: Your lender will ask for proof of your hardship. This might include:

- Pay stubs

- Bank statements

- Tax returns

- A letter explaining your situation

- Fill Out an Application: They will send you papers to complete. Fill them out fully and truthfully. Include all requested documents.

- Seek Expert Advice: Talk to a housing counselor approved by the Department of Housing and Urban Development (HUD). These counselors offer free or low-cost help. They can explain all your options. They can also help you talk to your lender. You can find local HUD-approved counselors on their website. An experienced real estate attorney can also guide you.

- Follow Up: Stay in touch with your lender. Make sure they received your documents. This process can take weeks or months. Ensure you meet all deadlines.

Conclusion

A deed in lieu of foreclosure is a way to handle a difficult mortgage situation. It lets you give your home to your lender. This helps you avoid a long and public foreclosure. While it affects your credit, it is often less damaging than a full foreclosure. Always understand all your options. Talk to experts to make the best choice for your unique situation.Frequently Asked Questions

Quick answers to the questions people ask most.How long does a deed in lieu of foreclosure take?

The process for a deed in lieu typically takes 3 to 12 months. This depends on your lender and how quickly you provide documents. It is usually faster than a full foreclosure.What is the difference between a deed in lieu and foreclosure?

A deed in lieu is when you willingly give your home to the lender. Foreclosure is when the lender forces you out through a legal process. A deed in lieu is often faster, less public, and less damaging to your credit.How bad does a deed in lieu of foreclosure hurt your credit?

A deed in lieu lowers your credit score, usually by 50 to 150 points. This is less than a full foreclosure, which can drop your score by over 100-200 points. It stays on your report for about seven years.Is a deed in lieu of foreclosure bad?

A deed in lieu is not ideal, as it means losing your home. However, it can be a "less bad" option compared to foreclosure. It offers a quicker, more private way to move on from debt.What are alternatives to a deed in lieu of foreclosure?

Other options to avoid foreclosure include:- Short Sale: Selling your home for less than you owe, with lender approval.

- Loan Modification: Changing your loan terms to make payments easier.

- Repayment Plan: Paying back missed payments over time.

- Forbearance: Taking a break from payments for a set period.