If you're worried about a late mortgage payment, you have choices. Lenders usually won't 'forgive' a payment. But many programs can help you pause or lower payments for a short time. These include forbearance, repayment plans, and loan changes. Act quickly and talk to your mortgage company. This guide tells you how to get help. It also explains what to do when payments are late, especially for Detroit homeowners.

Key Takeaways

- Forgiveness is Rare: True late mortgage payment forgiveness is uncommon. Lenders mostly offer temporary payment help.

- Act Fast: Contact your lender as soon as you think you might miss a payment.

- Forbearance: This lets you pause or lower payments temporarily. You must pay this money back later.

- Other Programs: Options like repayment plans, loan modifications, and payment deferrals can help.

- Hardship Matters: Lenders will ask about why you can't pay. Common reasons include job loss or illness.

- Foreclosure Takes Time: You won't lose your home right away. There are many steps and months before final foreclosure.

- Seek Help: HUD-approved housing counselors offer free help.

What Happens When You Can't Make Your Mortgage Payment?

Even one missed payment can cause problems, so act fast. Missing a mortgage payment can feel scary. But do not panic. Many lenders know that life sometimes brings problems. You might face late fees and credit score drops. Talking to your lender right away is important. Most mortgage companies give you a grace period. This is often 10 to 15 days after your due date. If you pay within this time, you usually do not get a late fee. After that, expect a fee. This fee is often 4% to 5% of your past-due payment. For example, on a $1,500 payment, a 4% fee adds $60. Late payments also hurt your credit score. This makes it harder to get new loans. A single late payment can drop your score by over 50 points. Over time, several late payments could lead to foreclosure. This is when the bank takes back your home. We help homeowners avoid foreclosure and sell a house quickly if needed. The Consumer Financial Protection Bureau (CFPB) shows that lenders prefer keeping you in your home. They have programs to help. These programs can offer ways to catch up on payments.Will a Mortgage Company Forgive a Late Payment?

It is rare for a mortgage company to forgive a late payment completely. They usually offer temporary help or adjust your payment plan. True "forgiveness" for a missed mortgage payment is uncommon. This means your lender will not just erase what you owe. You are still responsible for the full mortgage amount. They expect you to pay back all missed amounts. However, lenders can sometimes forgive late fees. This happens if you mostly pay on time. They might do it if this is your first late payment. You need to call your lender quickly to ask about it. Being proactive can help avoid extra charges. For example, if you pay late once in 10 years, they might waive the typical $50 fee. Most help comes as temporary payment changes. These are not true forgiveness. They might let you skip payments for a short time. You will still need to pay these amounts later. These options include:- Forbearance: This lets you pause or lower payments for a short time. You must pay back the missed amounts when the forbearance ends.

- Repayment Plan: You make extra payments each month to catch up. For instance, you add $100 to your regular payment for six months.

- Loan Modification: This changes your loan terms to make payments more affordable. This might mean a lower interest rate or a longer loan term.

Mortgage Forbearance: Your Temporary Payment Pause

Mortgage forbearance lets you pause or lower your payments for a short time, but you still need to pay back those amounts later. Mortgage forbearance is a helpful program. It lets you stop or reduce your mortgage payments for a set period. This can be 3 to 12 months. It gives you time to get back on your feet during hard times. Remember, this is not loan forgiveness. You will still owe all the money you paused or reduced. You must ask your mortgage company for forbearance. It does not happen automatically. Contact your mortgage servicer right away if you are struggling. They can explain your options. They will tell you what information you need to provide. To get forbearance, you usually need to show a hardship. Common reasons include:- Job loss

- Illness or medical bills

- Divorce or separation

- Death of a co-borrower

Understanding Forbearance Repayment Options

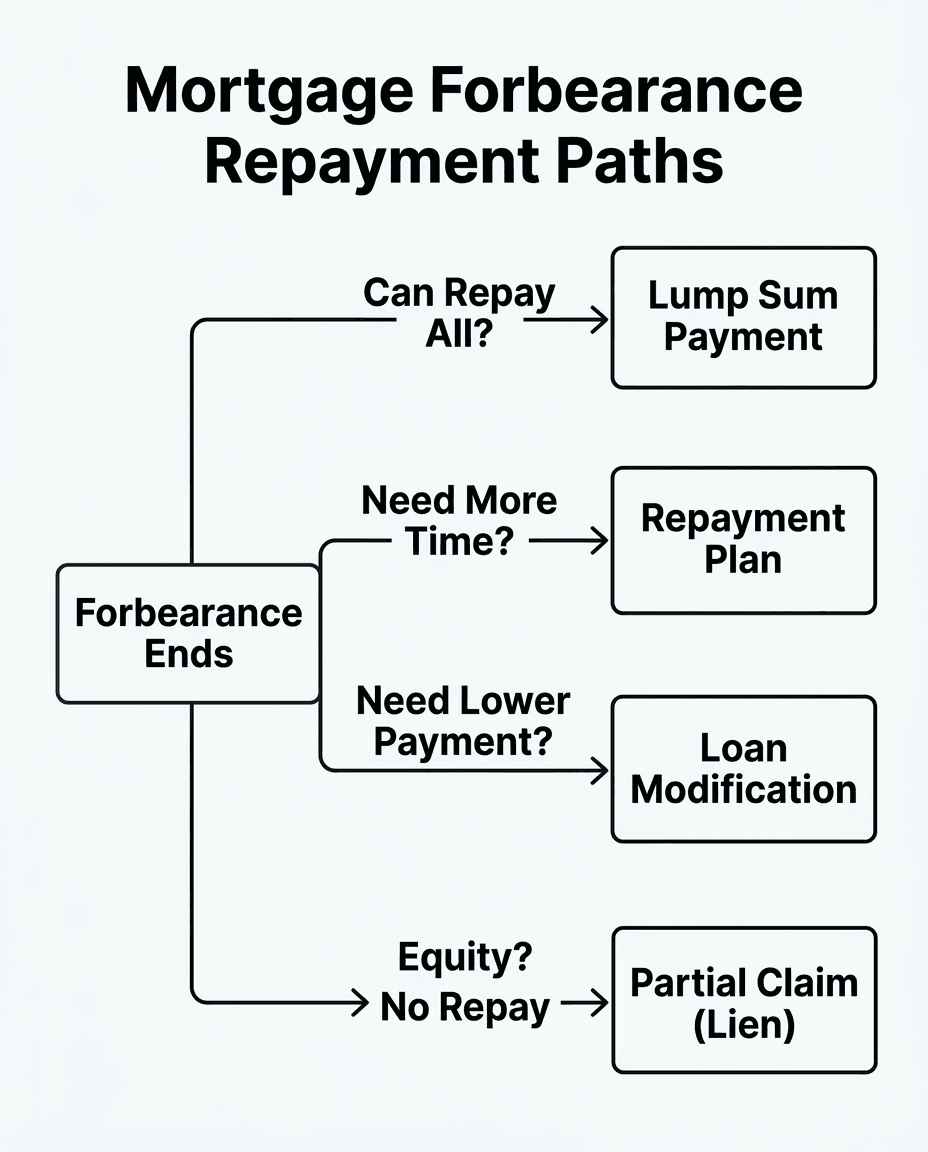

It's vital to know how you will repay your missed mortgage payments after a forbearance plan ends.

Flowchart outlining common mortgage forbearance repayment options like lump sum, repayment plan, loan modification, and partial claim.

When you pause your mortgage payments, those payments do not disappear. You will still need to pay them back. Knowing your repayment options is crucial. This helps you pick the best path for your situation.

There are a few main ways to repay missed payments. Each has different effects on your finances.

- Lump Sum Payment: This means paying back all missed payments at once. For example, if you missed four payments of $1,200 each, you would owe $4,800. This option can be hard for many homeowners.

- Repayment Plan: Your lender might let you add extra money to your regular payments. This spreads the missed amount over several months. For instance, you might add $200 to your $1,200 payment for 24 months. This makes your new payment $1,400.

- Payment Deferral or Partial Claim: This is often a good choice for Detroit homeowners. Your missed payments are moved to the end of your loan. This means your loan period gets longer. For example, if your loan was set to end in 2040, it might now end in 2041. You do not pay interest on this deferred amount. You typically repay it when you sell the home or pay off the main loan. The FHA's Loss Mitigation Program offers a "Partial Claim" option.

- Loan Modification: This changes the original terms of your mortgage. This might mean a lower interest rate or a longer repayment period. This can reduce your monthly payment. A full modification might change your total loan amount or term.

What is Considered a Hardship for a Mortgage?

When life throws a curveball, a "hardship" means something happened that makes it tough to pay your mortgage. A hardship is any big life event. It makes it hard or impossible for you to pay your house loan. Mortgage companies understand that sometimes things happen beyond your control. They often want to help you stay in your Grosse Pointe home if they can. You will need to explain your situation to your mortgage company. Be clear and honest. They want to know why you cannot make your payments right now. This helps them find the best solution for you. Common reasons that count as a hardship:- Job Loss: You or a family member lost a job. This is especially true if it impacts your household income.

- Serious Illness or Injury: A major health issue can lead to large medical bills or lost work time.

- Divorce or Separation: Ending a marriage can greatly change your financial picture.

- Death in the Family: Losing a loved one can mean less income or new costs.

- Natural Disaster: Fires, floods, or other events can damage your home or force you to move.

- Military Deployment: Being called to active duty can change your finances.

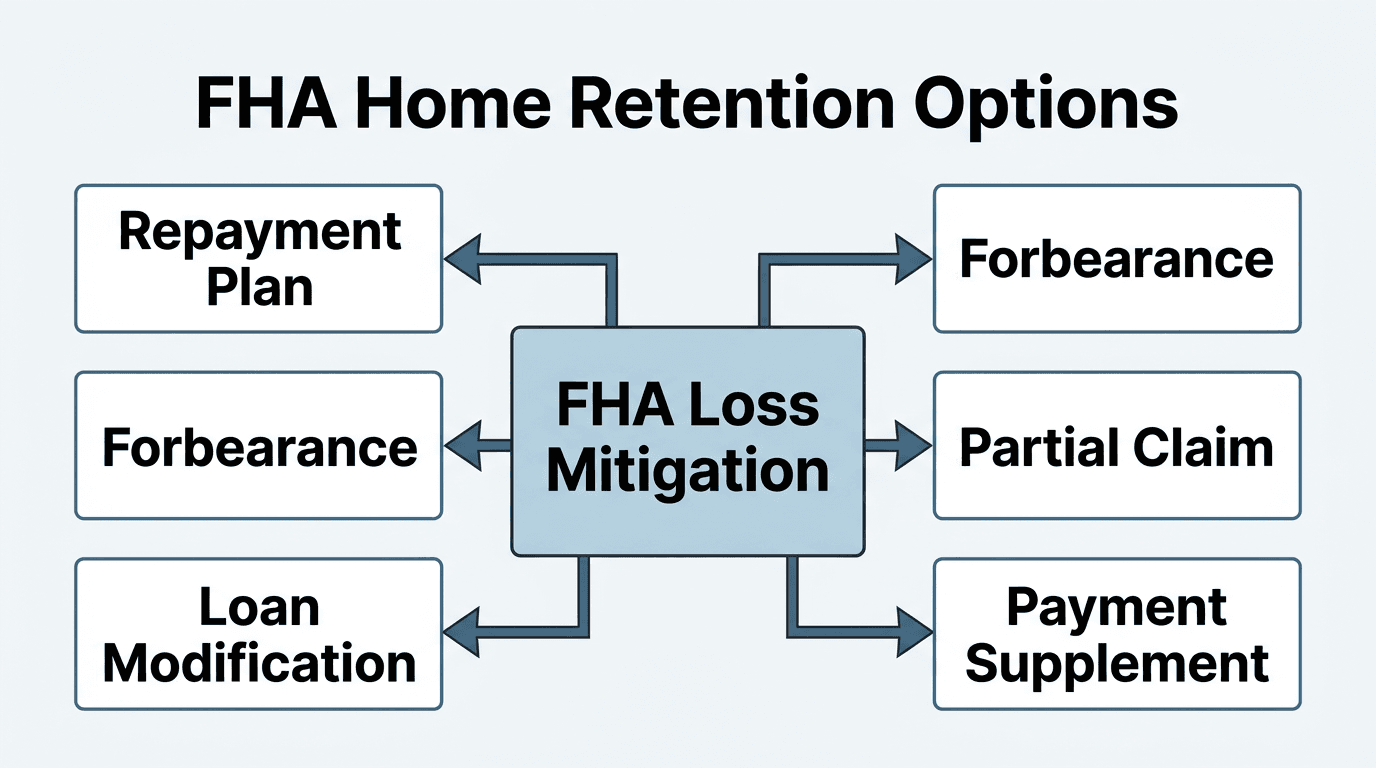

Other FHA Loss Mitigation Programs and Options

The Federal Housing Administration (FHA) offers programs beyond forbearance to help you keep your home in Detroit, Sterling Heights, or St. Clair Shores. The FHA has other ways to help you. These plans aim to make your monthly mortgage payments easier to manage. They can help if you are behind or worried about future payments. Always talk to your mortgage company about all your options.

Diagram showing FHA's various home retention options, including repayment plans, forbearance, partial claims, loan modification, and payment supplements.

Here are some FHA programs:

- Repayment Plan: This plan helps you catch up on missed payments. You pay a bit extra each month until you are caught up. Your mortgage company adds the past-due amount to your regular payment for a set time.

- Special Forbearance: This lets you stop or reduce payments for a while. It's for short-term problems. You must agree on how you will pay back the missed amounts later.

- Standalone Partial Claim: The FHA can pay some of your missed mortgage payments. They give your lender money to cover what you owe. You then pay this money back to the FHA. This payment does not start until your mortgage is paid off or you sell the house. Learn more about FHA's loss mitigation programs.

- Standalone Loan Modification: This changes the terms of your loan. It may lower your interest rate or extend your loan period. This reduces your monthly payment. This is a permanent change to your mortgage contract.

- Combination Loan Modification and Partial Claim: This option combines two solutions. It changes your loan terms and the FHA pays part of your missed payments. This helps many homeowners struggling to pay.

Can You Lose Your House for Late Payments?

Consistently missing mortgage payments can lead to foreclosure, but you have time to act. Yes, you can lose your home if you do not make your mortgage payments. This process is called foreclosure. It means the lender takes back your home to cover the money you owe. This is not a fast process. Foreclosure takes many months. Lenders do not want to take your house. They would rather you keep paying. You will get many notices and warnings before you lose your home. Here's how a foreclosure often works:- Missed Payments: You miss one or more monthly payments.

- Default: After 30 days, your loan is officially in "default." You may get late fees.

- Notice of Default: Your lender sends a letter. It says you are behind on payments. It also says how to catch up. This often happens after 90 days of missed payments.

- Acceleration: Your lender demands the full loan amount right away. This can happen around 120 days after your first missed payment.

- Foreclosure Sale: If you do not pay, your home goes up for sale.

How many months can you miss before losing your Detroit home?

Many people in Detroit, Sterling Heights, or St. Clair Shores worry about losing their homes. You will not face eviction right away if you miss a mortgage payment. Eviction only happens after your home is sold at a foreclosure auction. It takes time for foreclosure to begin. Lenders typically wait until you are 90 to 120 days behind on payments. This means you will likely miss at least three monthly payments before the official process starts. During this time, lenders will send notices. They want to avoid foreclosure too. Michigan law also provides specific steps and timeframes for foreclosure. You get important notices and a chance to respond. You have time to work with your lender on a plan. Solutions like forbearance can often help you catch up. We can help homeowners sell a house fast for cash if they cannot avoid foreclosure. For more help, the U.S. Department of Housing and Urban Development (HUD) offers resources for Michigan residents. Think of it this way:- 1-2 months missed: You may get late fees. Your credit score might drop a little.

- 3-4 months missed: The lender usually starts the foreclosure process. This is when official letters begin.

- After foreclosure sale: Only then can an eviction happen. This is a separate legal step.

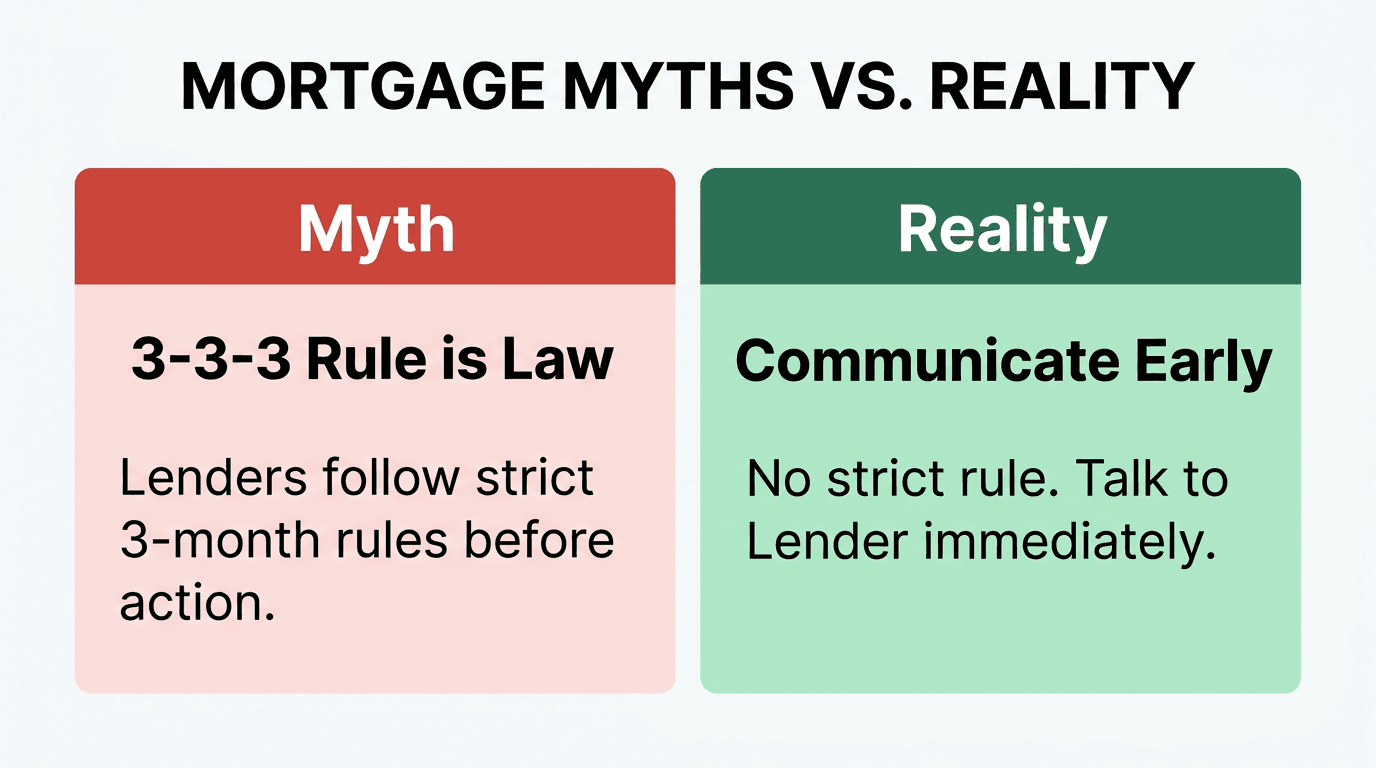

The 3-3-3 Rule for Mortgages (and Why It's Misleading)

You might hear about a "3-3-3 rule" for mortgages, but it's not a real policy.

Infographic debunking the 3-3-3 rule for mortgages, contrasting the myth with the reality of early communication.

You may have heard of a "3-3-3 rule" for mortgages. This idea suggests there is a strict timeline for missed payments. For example, some think it means you have three months before serious action. Others believe it relates to three calls or three warning letters.

However, the "3-3-3 rule" is not an official mortgage guideline or policy. It is a common misunderstanding. Mortgage companies do not follow a set "3-3-3 rule." Each lender has its own process for late payments.

Relying on such unproven "rules" can be very risky for your home. Instead of guessing, always talk directly with your mortgage company. They can tell you your exact options and what steps to take. Learn more about how selling your house for cash works if you need to act quickly.

Being proactive helps avoid bigger problems. For example, if you live in Detroit, Michigan, and are worried about falling behind, contacting your servicer early is key. Waiting too long can lead to more serious issues. The Consumer Financial Protection Bureau (CFPB) offers resources to help you understand your rights and options when facing mortgage payment difficulties. Talking to your servicer as soon as possible is their main advice.

Can You Defer a Mortgage Payment for One Month?

It's often possible to defer one mortgage payment, usually by adding it to the end of your loan. Yes, you can often defer a single mortgage payment. This means you skip one payment now. That missed payment is then added to the very end of your loan term. This extends your loan by one month. For instance, if your loan ends in December 2040, it would then end in January 2041. Your lender must agree to this plan. They typically review your payment history and current situation. A good reason, like a brief job loss or unexpected car repair, helps. This option is helpful for short-term money troubles. It keeps you from having a late payment mark on your credit report. This differs from mortgage forbearance, which lets you pause payments for a longer time. If you need to sell a house fast due to money issues, we can help.Behind on Mortgage Payments in Detroit, Sterling Heights, or St. Clair Shores? Get Help Now

It's important to act quickly if you fall behind on payments, and local experts can help you understand your options. If you live in Detroit, Sterling Heights, or St. Clair Shores and are struggling with your mortgage, free help is available. HUD-approved housing counselors offer expert advice. They can review your situation and talk to your lender for you. These services can be a lifesaver. Here are some local housing counseling agencies:- U-SNAP-BAC, Inc. website link: Located in Detroit, they assist with foreclosure prevention.

- Detroit Urban League: This group offers various housing support services.

Selling Your Home as an Alternative to Foreclosure

If you face foreclosure, selling your Detroit-area property can prevent lasting damage to your finances. Sometimes, even with help options, keeping your home is not possible. Selling your home before foreclosure happens can protect your credit score. It can also help you avoid the stress of a forced sale. You get to control the sale process. You might hear about a "pre-foreclosure sale." This is when you sell your home before the bank takes it. Another option is a "Deed-in-Lieu of Foreclosure." This means you give your home's deed back to the lender. Both avoid a full foreclosure on your record. At HouseGoodbye, we offer a fast and easy way to sell your house. We buy houses for cash in places like Birmingham, MI, Sterling Heights, MI, and St. Clair Shores, MI. You get a fair cash offer quickly. This lets you pay off your mortgage debt and move on. Many homeowners facing tough times, like divorce or downsizing, choose this path. Learn more about selling a house fast for cash.Can I Get a 700 Credit Score with Late Payments?

It's tough to get a good credit score if you've paid your mortgage late, but you can improve it over time. Late payments really hurt your credit score. If you miss a mortgage payment, your score can drop a lot. For example, a single 30-day late payment could drop a 780 score by 90 to 110 points. A late payment stays on your credit report for seven years. This makes it hard to reach a 700 credit score, especially if the late payment is recent. Lenders see these as a sign of risk. To improve your score, focus on these steps:- Pay on time. Make all future payments, for all your debts, on time.

- Lower your debts. Try to pay down credit card balances.

- Check your report. Review your credit report often for errors. You can get a free report each year. Find your credit report here.